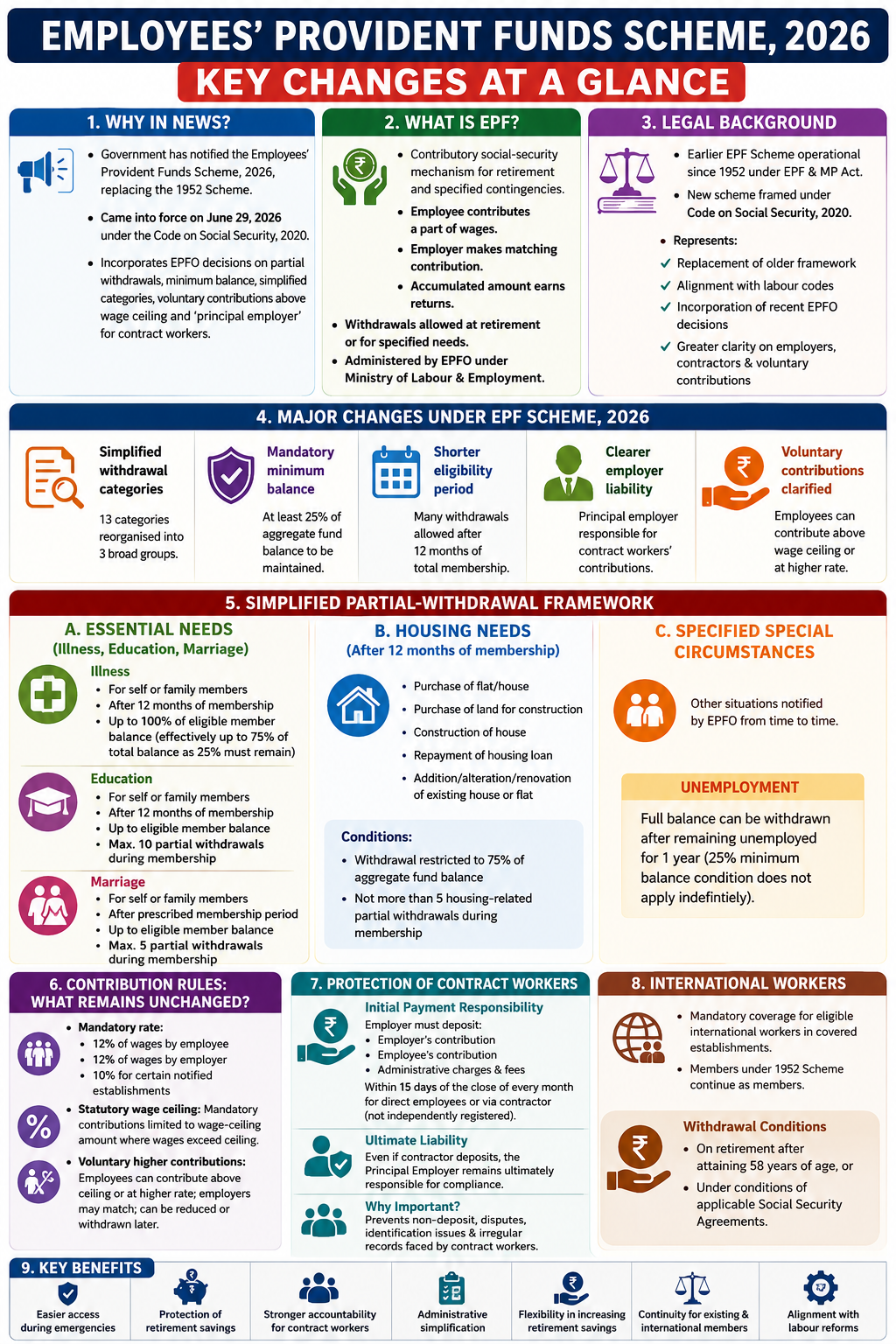

Why in News?

- The Union government has notified the Employees’ Provident Funds Scheme, 2026, replacing the Employees’ Provident Funds Scheme, 1952.

- The new scheme came into force on June 29, 2026, as part of the implementation of the Code on Social Security, 2020.

- It incorporates recent EPFO decisions relating to partial withdrawals, the compulsory maintenance of a minimum balance and simplified withdrawal categories. It also explicitly provides for voluntary contributions above the statutory wage ceiling and introduces the concept of a principal employer for contract workers.

What is the Employees’ Provident Fund?

The Employees’ Provident Fund is a contributory social-security mechanism intended to provide workers with financial support after retirement or during specified contingencies.

Under the system:

- The employee contributes a prescribed proportion of wages.

- The employer makes a matching contribution.

- The accumulated amount earns returns.

- Withdrawals are permitted at retirement or for specified needs subject to conditions.

The scheme is administered by the Employees’ Provident Fund Organisation, under the Ministry of Labour and Employment.

Legal Background of the New Scheme

The earlier EPF Scheme had been operating since 1952 under the Employees’ Provident Funds and Miscellaneous Provisions Act.

The new scheme has been framed under the broader architecture of the Code on Social Security, 2020, which seeks to consolidate and rationalise various labour-related social-security laws.

The EPF Scheme, 2026 therefore represents:

- Replacement of an older statutory framework

- Alignment with the labour codes

- Incorporation of recent EPFO policy decisions

- Greater clarity regarding employers, contractors and voluntary contributions

Major Changes under the EPF Scheme, 2026

Simplified withdrawal categories:

The earlier 13 categories of partial withdrawals have been reorganised into three broad groups:

- Essential needs

- Housing needs

- Specified special circumstances

Mandatory minimum balance:

Members must generally maintain at least 25% of the aggregate fund balance in their EPF account.

Shorter eligibility period:

Many partial withdrawals are permitted after completing 12 months of total fund membership.

Clearer employer liability:

The responsibility of the principal employer for contributions relating to contract workers has been explicitly recognised.

Voluntary contributions clarified:

Employees can contribute above the statutory wage ceiling or at a rate exceeding the mandatory contribution rate.

Simplified Partial-Withdrawal Framework

Essential Needs

The essential-needs category covers illness, education and marriage.

Illness

A member may withdraw funds for the illness of:

- Self

- Eligible family members

The withdrawal may be made after completing 12 months of total membership.

A member can withdraw up to 100% of the eligible member balance.

However, because at least 25% of the total balance must remain in the account, the maximum ordinarily available is effectively 75% of the aggregate fund balance.

Education

Members may withdraw for the education of:

- Self

- Eligible family members

The conditions include:

- Completion of 12 months of membership

- Withdrawal up to the eligible member balance

- A maximum of 10 partial withdrawals during the entire membership period

Marriage

A member may withdraw for the marriage of:

- Self

- Eligible family members

The conditions include:

- Completion of the prescribed membership period

- Withdrawal up to the eligible balance

- A maximum of five partial withdrawals during the membership period

Housing Needs

Partial withdrawal is permitted for:

- Purchase of a residential flat or house

- Purchase of land for construction

- Construction of a house

- Repayment of a housing loan

- Addition, alteration or renovation of an existing house or flat

The principal conditions are:

- At least 12 months of total membership

- Withdrawal restricted to 75% of the aggregate fund balance

- Not more than five housing-related partial withdrawals during membership

The simplified housing category combines several earlier sub-categories into one broader framework.

Withdrawal during Unemployment

The compulsory 25% minimum balance does not apply indefinitely in cases of prolonged unemployment.

A member may withdraw the entire EPF balance after remaining unemployed for one year, subject to the prescribed procedure.

This provision balances:

- Immediate financial support during unemployment

- Preservation of some retirement savings during shorter employment gaps

Contribution Rules: What Remains Unchanged?

Mandatory rate

The prescribed contribution rate continues to be:

- 12% of wages by the employee

- 12% of wages by the employer

For certain notified establishments, the contribution rate continues to be 10%.

Statutory wage ceiling

Where wages exceed the statutory ceiling, mandatory contributions are ordinarily restricted to the wage-ceiling amount.

Thus, the new scheme does not automatically make contribution on the entire salary compulsory.

Voluntary higher contributions

Employees may choose to:

- Contribute on wages exceeding the statutory ceiling, or

- Contribute at a rate higher than 12%

Employers may also choose to make matching contributions.

These additional voluntary contributions may later be reduced or discontinued by the employee or employer.

The provision provides flexibility to individuals who wish to increase retirement savings without imposing a fresh universal obligation.

Protection of Contract Workers

A significant feature of the new scheme is the explicit recognition of the principal employer.

Initial payment responsibility

The employer must deposit:

- The employer’s contribution

- The employee’s contribution

- Applicable administrative charges and fees

This must generally be completed within 15 days of the close of every month for workers employed directly or through a contractor who is not independently registered.

Ultimate liability

Where a contractor deposits the provident-fund contribution, the principal employer remains ultimately responsible for ensuring compliance.

This provision is important because contract workers frequently face:

- Non-deposit of deducted contributions

- Disputes between contractors and establishments

- Difficulty in identifying the responsible employer

- Irregular employment records

The new scheme seeks to prevent employers from avoiding social-security obligations by outsourcing labour.

Provisions for International Workers

The EPF Scheme, 2026 retains mandatory coverage for eligible international workers employed in covered establishments.

It also clarifies that international workers who were members under the 1952 Scheme will continue as members under the new framework.

Withdrawal conditions

International workers are generally permitted to withdraw their funds:

- On retirement after attaining 58 years of age, or

- Under conditions provided through applicable Social Security Agreements

This ensures continuity of rights while recognising India’s bilateral social-security arrangements with other countries.

Significance of the New Scheme

Easier access during emergencies:

- Simplified withdrawal categories reduce procedural confusion and make funds more accessible during illness, education, marriage and housing needs.

Protection of retirement savings:

- The 25% minimum-balance rule seeks to prevent complete depletion of the provident fund through repeated partial withdrawals.

Greater accountability:

- The principal-employer provision strengthens the protection of contract workers.

Administrative simplification:

- Consolidating multiple withdrawal categories can reduce documentation and processing delays.

Flexibility in savings:

- Voluntary higher contributions allow workers to build a larger retirement corpus according to their financial capacity.

Legal continuity:

- Existing members, including international workers, continue under the new scheme without disruption.

Alignment with labour reforms:

- The framework brings provident-fund regulation in line with the Code on Social Security, 2020.

Key Concerns

Retirement-corpus erosion:

- Even with a 25% reserve, frequent withdrawals may significantly reduce long-term savings.

Limited adequacy of minimum balance:

- Retaining only one-fourth of the corpus may be insufficient for retirement, particularly for workers with low or irregular contributions.

Contract-worker enforcement:

- The principal-employer rule will be effective only if inspection, digital verification and grievance mechanisms are strengthened.

Awareness deficit:

- Workers may not understand the difference between total balance, eligible balance and voluntary contributions.

Digital exclusion:

- Workers with limited digital literacy may face difficulties in filing claims or correcting employment records.

Employer compliance:

- Delayed remittances and incorrect wage reporting may continue unless penalties and monitoring are effective.

Short-term versus long-term needs:

- The scheme must balance emergency liquidity with the central purpose of retirement security.

Way Forward

- Provide clear multilingual guidance on withdrawal limits and eligible balances.

- Send real-time alerts to employees whenever contributions are deposited.

- Allow workers to verify contractor and principal-employer compliance digitally.

- Strengthen grievance redressal for delayed or missing contributions.

- Introduce financial counselling before high-value withdrawals.

- Ensure portability of records across employers and contractors.

- Use data analytics to identify establishments with repeated defaults.

- Protect informal and low-wage workers from unauthorised deductions.

- Simplify claim processing without weakening verification.

- Periodically assess whether the 25% minimum balance adequately protects retirement security.

Conclusion

The Employees’ Provident Funds Scheme, 2026 modernises India’s provident-fund framework by simplifying withdrawals, clarifying contribution rules and strengthening accountability for contract workers.

Its worker-friendly withdrawal provisions can provide timely financial relief. However, provident-fund savings remain primarily a source of retirement protection.

The scheme’s success will therefore depend on maintaining a careful balance between present financial needs, employer accountability and long-term social security.