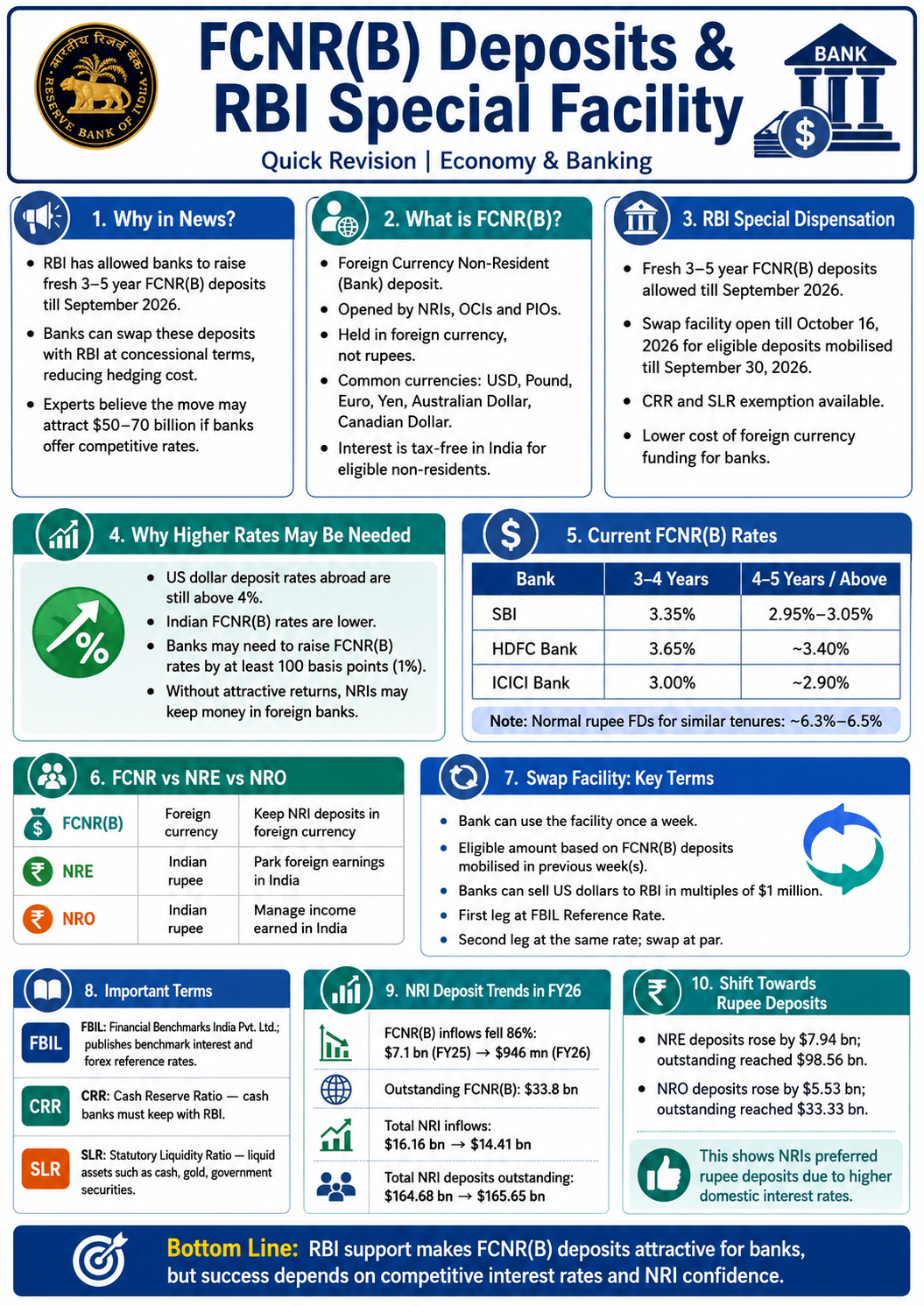

Why in News?

The Reserve Bank of India has announced a special facility allowing banks to mobilise fresh three- to five-year Foreign Currency Non-Resident (Bank) deposits, or FCNR(B) deposits, until September 2026.

The RBI has also allowed banks to swap these deposits with the central bank at a concessional rate. This means the RBI will effectively absorb the hedging cost, making FCNR(B) deposits a more attractive overseas funding source for Indian banks.

Experts believe the move may attract around $50 billion to $70 billion in additional foreign capital, provided banks offer competitive interest rates to Non-Resident Indians.

What are FCNR(B) Deposits?

- FCNR(B) stands for Foreign Currency Non-Resident (Bank) deposits.

- These are fixed-term bank deposits opened in India by:

- Non-Resident Indians

- Overseas Citizens of India

- Persons of Indian Origin

- These deposits are maintained in foreign currencies such as:

- US dollar

- Pound sterling

- Euro

- Japanese yen

- Australian dollar

- Canadian dollar

- Unlike normal rupee deposits, FCNR(B) deposits are held in foreign currency.

- Interest earned on FCNR(B) deposits is exempt from income tax in India as long as the depositor qualifies as a non-resident under Indian tax laws.

RBI’s Special Dispensation

- Banks can mobilise fresh three- to five-year FCNR(B) deposits until September 2026.

- Banks can swap these foreign currency deposits with the RBI at a concessional rate.

- The swap facility will remain open up to October 16, 2026 for eligible deposits mobilised until September 30, 2026.

- Banks are exempted from maintaining Cash Reserve Ratio and Statutory Liquidity Ratio on these deposits.

- This reduces the cost of raising foreign currency resources for banks.

Why Higher Interest Rates May Be Needed

The RBI’s support reduces hedging costs for banks, but it may not be enough to attract large NRI inflows.

- US dollar deposit rates in major markets are still above 4%.

- Indian banks currently offer lower rates on FCNR(B) deposits.

- Bankers believe Indian banks may need to raise FCNR(B) rates by at least 100 basis points.

- 100 basis points = 1 percentage point.

- Without attractive rates, NRIs may prefer to keep their deposits in foreign banks.

- Therefore, regulatory support must be combined with competitive pricing.

Current FCNR(B) Deposit Rates

FCNR(B) rates are lower than regular rupee fixed deposit rates because they are linked to foreign currency interest rate conditions.

| Bank | FCNR(B) Rate for 3–4 Years | FCNR(B) Rate for 4–5 Years / Above |

| SBI | 3.35% | 2.95% to 3.05% |

| HDFC Bank | 3.65% | Around 3.40% |

| ICICI Bank | 3.00% | Around 2.90% |

In comparison, normal rupee fixed deposits for similar tenures offer around 6.3% to 6.5%.

Difference Between FCNR(B), NRE and NRO Accounts

| Account Type | Currency | Main Purpose |

| Foreign Currency Non-Resident (Bank) – (FCNR) Account | Foreign currency | To keep NRI deposits in foreign currency |

| Non-Resident External– (NRE) Account | Indian rupee | To park foreign earnings in India |

| Non-Resident Ordinary– (NRO) Account | Indian rupee | To manage income earned in India |

New Swap Facility: Terms and Conditions

- A bank can use the swap facility only once in a week.

- The maximum amount a bank can swap will be equal to eligible FCNR(B) deposits mobilised during the previous week or weeks.

- Banks can sell US dollars to the RBI in multiples of $1 million.

- Banks will simultaneously agree to buy back the same amount of dollars at the end of the swap period.

- In the first leg, banks will sell dollars to the RBI at the FBIL Reference Rate.

- The second leg will take place at the same rate.

- The swap will be undertaken at par.

What is FBIL?

- FBIL stands for Financial Benchmarks India Private Limited.

- It publishes benchmark interest rates and foreign exchange reference rates for Indian financial markets.

- The FBIL Reference Rate is used for foreign exchange-related transactions.

What are CRR and SLR?

Cash Reserve Ratio

- CRR is the minimum percentage of deposits banks must keep with the RBI as cash.

- Banks cannot lend this amount.

Statutory Liquidity Ratio

- SLR is the minimum percentage of deposits banks must maintain in liquid assets such as:

- Cash

- Gold

- Government securities

- Exemption from CRR and SLR improves the attractiveness of FCNR(B) deposits for banks.

NRI Deposit Trends in FY26

- FCNR(B) deposit inflows fell sharply by 86% in FY26.

- Inflows declined from $7.1 billion in FY25 to $946 million in FY26.

- Outstanding FCNR(B) deposits stood at $33.8 billion at the end of March.

- Total NRI deposit inflows also declined from $16.16 billion in FY25 to $14.41 billion in FY26.

- Total NRI deposits outstanding rose slightly from $164.68 billion to $165.65 billion.

Shift Towards Rupee Deposits

Although FCNR(B) inflows declined, NRE and NRO deposits increased.

- NRE deposits rose by $7.94 billion in FY26.

- NRE outstanding deposits reached $98.56 billion.

- NRO deposits rose by $5.53 billion.

- NRO outstanding deposits reached $33.33 billion.

This shows that NRIs preferred rupee-denominated deposits because domestic interest rates were more attractive.

Significance

- Helps attract foreign currency deposits from NRIs.

- Supports foreign exchange reserves and external sector stability.

- Provides banks with overseas funding.

- Can help stabilise the rupee during external pressure.

- Reduces hedging cost for banks.

- Encourages NRI participation in India’s financial system.

- Supports liquidity and credit availability in the banking system.

Challenges

- FCNR(B) rates are currently lower than overseas dollar deposit rates.

- Higher rates may be needed to attract NRI funds.

- If banks raise rates too much, their cost of funds may increase.

- Foreign currency deposits carry exchange rate and maturity management concerns.

- Inflows may remain weak if global interest rates stay high.

- NRIs may prefer NRE and NRO deposits if rupee returns remain attractive.

- The facility may provide only temporary support unless rates become competitive.

Way Forward

- Banks should offer competitive FCNR(B) rates after factoring in RBI’s hedging support.

- Deposit pricing should balance depositor attraction and bank profitability.

- RBI should monitor foreign currency liquidity and exchange rate risks.

- Banks should promote FCNR(B) deposits among NRIs through transparent communication.

- India should strengthen long-term foreign capital inflows beyond temporary deposit schemes.

- External sector stability should be supported through exports, remittances, FDI and prudent debt management.

Conclusion

The RBI’s special FCNR(B) deposit swap facility is aimed at encouraging NRI dollar inflows and improving foreign currency liquidity. By absorbing hedging costs and exempting banks from CRR and SLR requirements, the RBI has made these deposits more attractive for banks.

However, the success of the move depends on whether banks offer competitive interest rates. With overseas dollar deposits still giving returns above 4%, Indian banks may need to raise FCNR(B) rates meaningfully. A balanced approach is needed to attract NRI funds, support external stability and protect bank margins.